The Potential of CBDCs in Modern Economies

An Introduction to Central Bank Digital Currencies

Central Bank Digital Currencies (CBDCs) are emerging as a transformative force in digital finance, reshaping how we interact with money. These digital versions of national currencies, issued and regulated by central banks, promise to redefine financial systems by offering a state-backed alternative to both physical cash and cryptocurrencies. Unlike traditional forms of money, CBDCs leverage advanced technology to facilitate secure, efficient, and real-time transactions. Their introduction could mark a pivotal shift in economic frameworks, driving innovation and potentially altering the dynamics of global finance.

The Benefits of CBDCs for Today's Economies

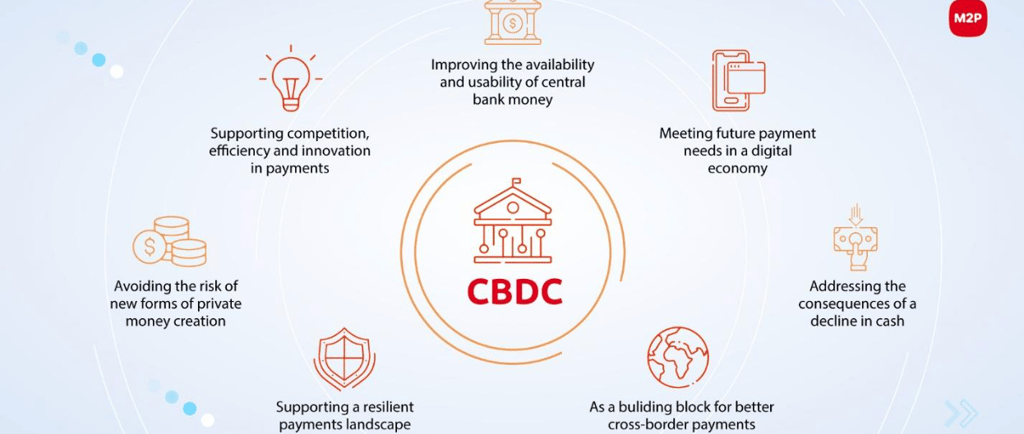

CBDCs offer several key benefits for modern economies. They have the potential to significantly enhance financial inclusion by making digital currency accessible through smartphones and digital wallets, reaching populations that are currently unbanked. In addition, CBDCs can streamline payment systems, enabling real-time transactions and reducing the need for intermediaries. This can lower transaction costs, benefiting both consumers and businesses. Moreover, the use of CBDCs can improve the efficiency of monetary policy implementation, giving central banks better tools to manage economic stability. These advantages highlight the transformative potential of CBDCs in reshaping financial systems.

CBDCs' Role in Promoting Economic Stability

CBDCs have the potential to refine monetary policy by providing central banks with direct insights into money flows, enabling more precise and timely policy adjustments. This heightened control can help manage economic cycles and improve responses to financial crises. Additionally, CBDCs can aid in controlling inflation by offering real-time data on spending patterns, allowing for more accurate adjustments to interest rates. This closer alignment between money supply and economic conditions could contribute significantly to overall economic stability. However, to fully leverage these benefits, robust frameworks ensuring security and privacy are essential.

Security Issues and Obstacles

Security is a paramount concern when it comes to CBDCs. The digital nature of these currencies makes them susceptible to cyberattacks and hacking attempts, necessitating robust cybersecurity protocols. Additionally, privacy issues arise as transactions could be traceable by central authorities, leading to potential misuse of data. To address these concerns, it is vital to implement advanced encryption technologies and stringent data protection measures. Another obstacle is the need for a resilient infrastructure capable of handling large-scale transactions without downtime. Ensuring both security and privacy will be essential to gain public trust and widespread acceptance of CBDCs.

Global Developments and the Rise of CBDCs

Countries across the globe are actively exploring the potential of Central Bank Digital Currencies (CBDCs), signifying their growing role in modern financial systems. China is leading the charge with its digital yuan, while nations like Sweden and the Bahamas are advancing their initiatives. These efforts represent a pivotal shift towards integrating digital currencies into existing economic frameworks, highlighting the urgency for robust infrastructure and regulatory standards. As more countries embark on their CBDC journeys, the implications for international trade and financial relations become increasingly significant. This widespread exploration underscores the transformative potential of CBDCs, compelling governments to adapt and innovate to stay competitive in the evolving digital landscape.

Comparing CBDCs and Cryptocurrencies

While both CBDCs and cryptocurrencies operate in the digital realm, their foundational principles and operational structures differ substantially. CBDCs are state-backed and regulated by central banks, which provides a degree of stability and trust not typically associated with cryptocurrencies like Bitcoin. Cryptocurrencies, on the other hand, thrive on decentralization, offering users anonymity and freedom from traditional financial institutions. This fundamental difference means that while CBDCs aim to integrate smoothly into existing financial systems, cryptocurrencies often position themselves as alternatives or even disruptors to these systems. The dynamic interplay between these two forms of digital currency could lead to a more diversified and resilient financial landscape, offering a broader range of options for consumers and investors alike.

The Future of CBDCs in the Global Economy

The adoption of Central Bank Digital Currencies (CBDCs) is poised to create significant shifts in global economies. Their integration into the financial system could streamline banking operations and enhance monetary policy effectiveness, making economies more resilient to shocks. As CBDCs become more prevalent, they might also drive a wave of innovation in financial services, fostering greater competition and potentially lowering costs for consumers. However, this transition requires careful consideration of regulatory frameworks to ensure that security and privacy are adequately addressed. The interplay between CBDCs and other emerging financial technologies will be crucial in determining their long-term impact. For countries and financial institutions, staying ahead of these developments will be essential to harness the full potential of CBDCs and maintain a competitive edge in the digital age.

The landscape of Central Bank Digital Currencies (CBDCs) offers a compelling glimpse into the future of digital finance. Their ability to enhance financial inclusion, streamline payment systems, and provide more precise tools for economic stability makes them a noteworthy development in modern economies. However, the road to widespread adoption is fraught with challenges, particularly concerning security and privacy. Addressing these concerns is crucial for gaining public trust and ensuring the seamless integration of CBDCs into existing financial systems.

As countries around the world explore and implement CBDCs, it is evident that these digital currencies could significantly reshape the global economic landscape. This transformation demands robust regulatory frameworks and resilient infrastructures capable of supporting large-scale transactions. The potential for CBDCs to drive innovation in financial services cannot be overstated, promising new opportunities for consumers and businesses alike.

Navigating the future of CBDCs will require a careful balance of innovation and regulation. Stakeholders must remain vigilant, continuously adapting to the evolving technological and economic environment. The dynamic interplay between CBDCs and other digital currencies, such as cryptocurrencies, will further diversify and strengthen the financial ecosystem, offering a broader array of options for individuals and institutions.

In essence, the rise of CBDCs heralds a new era in digital finance, one that holds the promise of greater efficiency, inclusivity, and economic stability. By addressing the inherent challenges and leveraging the opportunities presented by CBDCs, modern economies can position themselves at the forefront of this digital revolution. As we move forward, staying informed and engaged with these developments will be paramount in harnessing the full potential of CBDCs in the global economy.

High Risk Investment Notice: Trading Crypto/Forex/CFDs carries a high level of risk and may not be suitable for all investors as you could sustain losses in excess of deposits. The products are intended for retail, professional and eligible counterparty clients. For clients who maintain accounts.

Address

Suite #194 1111 Davis Dr. Unit 23 Newmarket, ON L3Y 9E5